Read the peer reviews for this feature.

Read the peer reviews for this feature.

Download the graphs for this feature.

"Railway companies and city regions have conflicting objectives. It’s a major constraint,” says Richard Coburn, head of economic development at consultant Atkins.

“Railways want people to move around quickly. Get them in… get them on a train. Local stakeholders want people to stay and use new facilities, generate employment, improve communities. Rail has a singular task - it doesn’t need to deliver more than a railway.”

The railway owns large tracts of lucrative development land, often close to urban centres. It is wary about selling this land off, as future passenger growth means more sidings will be needed to stable more trains. What is useless wasteland today may not remain so, and must therefore be protected. But what remains is unsightly blight - acres of buddleia and rusting rubbish, often juxtaposed with smart new town centre developments.

“British Rail got quite good at selling off surplus land. And Railtrack was exceptionally good at it. By the time I got involved there wasn’t a huge amount of surplus land left,” says David Biggs, managing director, property, at Network Rail.

“We have in the region of 200 development ideas which range from the rebuilding of Twickenham station to a larger scheme using the car park at Manchester Victoria,” he adds.

“There are great examples of collaborative development,” counters Warwick Lowe, a former station manager who is now rail planning director at Atkins.

“King’s Cross, obviously. For the new Birmingham station, the railway chaired bodies with local stakeholders and worked out who was getting the value. The city gets a landmark structure that allows regeneration, so the city put some money in.”

Coburn adds: “On a smaller scale, Wolverhampton has ambitious plans to upgrade the station, reinvigorating a wider area. It’s a horrible station. It puts people off, especially women at night. Creating a new sense of place will increase the throughput of passengers.”

Case study: Argent and King’s Cross

The massive development of land around King’s Cross is the obvious place to start. Here we are talking in billions of pounds, which means it is far from typical of rail-related property developments.

When developer Argent moved in, most of the land was in one big parcel. And through London & Continental Railways, the Government retains a stake in it.

This is one of the biggest and best development sites in central London, on a scale like nothing else on the railway. Yet Argent had no expertise in railways - its job was to bring in big-money tenants such as the London headquarters of Google.

“Our relationship with the railway is excellent,” says Argent partner André Gibbs. But pressed harder, he admits: “It probably wasn’t the warmest at the beginning. I’m sure there was some suspicion about what we were trying to do, and it wanted to draw lines in the sand. Although Network Rail shared our vision for the area, it didn’t have an economic interest in it. We both knew we needed each other and although it wasn’t trusting at the beginning, it is now.”

Argent put £160 million into the site, and then used deals with the earliest occupiers to spend £330m on infrastructure. It is the developer’s biggest ever project. New roads had to be built. But although this is old railway land alongside two landmark London termini, the development fundamentally has little to do with the railway.

Says Gibbs: “In terms of how King’s Cross interacts with the public realm, we have helped make the new concourse which binds the station together and even more of a success. We also own the Great Northern Hotel, which helps to create a better station.

“Network Rail speak with pride about what they’ve achieved, but they also speak with pride about their role in the wider area. They have been a big part of that - they’ve got a halo effect from it.”

The whole area has benefited. British Transport Police points to a drop in crime, as the character of a formerly run-down quarter has changed. Prostitution and drug offences are substantially down.

“We didn’t set out to reduce crime on the railway,” points out Gibbs. “We did set out to make the area safe and clean. You don’t look at these things in the silos of the ownership boundaries. Improvements beyond our boundary improve our values, reduce our risk.”

Work to plan this new piece of London started in 2000. What was then known as the Channel Tunnel Rail Link was completed in 2007, so the following year was the earliest that commercial developers could move in. Construction will take until at least 2020, making it a 20-year project.

“We didn’t know what the market might be,” says Gibbs. “The site is next to one of the busiest railway stations in the UK. It’s a short walk to a train to Paris or Brussels and it’s in central London.

“So we needed a planning application with flexibility. The roads we put down will last for centuries, but we needed to be able to swing blocks from housing to commercial to retail as the market changed. We hadn’t imagined having a university in the middle of the site - we didn’t know the student housing block would be the first building occupied.

“We started work three months after Lehmans Brothers collapsed and the whole financial structure changed. But because we had a mix of business and residential uses we could invest all our money into infrastructure to get some momentum going, while the world around us sorted itself out.”

Who owns Argent? “Me and my friends,” says Gibbs. “Ten partners. Our investment at King’s Cross is done alongside the BT pension scheme.”

For years the ‘Next Big Project’ has been seen as nearby Euston. Argent wants to be involved.

“These opportunities come on the back of major infrastructure works, and they don’t come along very often,” says Gibbs.

“At Euston, HS2 will be the catalyst, and by then it will be long overdue. It’s important to bring specialist developers on board at an early stage, as it’s not easy for a rail operator to see how a development decision might be compromised.

“So don’t just have them on board as advisers - use people who will have to live with the consequences, who have to sell and let what is built.

“For example, at King’s Cross we were able to put infrastructure in place for Network Rail. We could put a road ramp into their station without that creating major legal access rights issues. That created simplicity of servicing, construction and delivery. Anyone doing a market plan off the back of a station plan needs the right expertise.”

Case study: Tavistock

On a completely different scale is the re-opening of the branch line from Bere Alston to Tavistock, a small market town in Devon with a population of 12,000.

For years, reinstatement of the route linking the town with Plymouth has been tied to an otherwise-unrelated plan to build 750 homes at Callington Road on the edge of the town. Outline planning consent was granted last September.

“We first came up with the idea in 2007,” explains Peter Frost, managing director of the developer, Kilbride. “So we’re looking at a total time for the scheme of around 15 years. But it’s the residential side that has taken the time, not the railway.”

In return for the housing deal, Kilbride promised that it would fund the re-opening of a route closed in 1968. Five and a half miles of track bed were found to be in mostly good condition and easily reinstated as a single-track route to a new station, offering an hourly service.

“We decided the best way to secure housing was to deliver good infrastructure at the same time,” Frost explains. “We looked at all the current and disused lines throughout Devon and Cornwall, and related them to the likely future housing allocations. We found that Tavistock was the largest town with no rail connection and an unresolved housing issue. The two were tied together from the start.”

Initially there was local opposition. But it was aimed at the new homes, not at the railway. Kilbride has since sold the housing development to Bovis Homes and formed Kilbride Community Rail. Preparation of the building land is likely in the second half of this year.

“We’re now discussing with Devon County Council the best way to deliver the railway,” says Frost. “You can go for a Development Consent Order for a national infrastructure project. Or you can go for a Transport & Works Act Order, which is slightly quicker. But either of these processes would be quite lengthy and detailed, so will take two to three years. Work could get under way three years from now at the earliest, with trains running 2019-2020.”

The line north from Bere Alston on the Gunnislake branch was not always an offshoot - it is the stub of the former London & South Western Railway route round Dartmoor, from Exeter to Plymouth via Okehampton. Following last year’s collapse of the main line along the sea wall at Dawlish, there is renewed interest in re-opening the remaining disused line as an alternative to the only rail route to Plymouth.

“The Dawlish influence has been positive,” asserts Frost. “Anything that raises the urgency of re-opening the line helps with the legal process. Because if we reinstate our five and a half miles, that leaves only 12 miles in the middle that need to be put back.

“Network Rail is at an early stage of looking at options. Some alternative to Dawlish is clearly going to be needed, and ours is a realistic option.”

When the planning approval came through last year, Nevin Holden of Bovis Homes hailed it as “a national blueprint for the delivery of new rail infrastructure”. Really? Nowhere else has got far with this approach.

“No one has tried a whole route,” concedes Frost. “Some stations have been opened as a result of residential development, though.

“The nearest idea is on a much larger scale - the East West Rail project. It has some similarities because it is linked to a series of developments through Bedfordshire towards Cambridge. They’ve identified similar housing allocations that can be tied in with contributions from the developers towards the reinstatement of the railway.

“But there, of course, the rail reinstatement has other drivers as well as the housing. It’s the rail project that came first, not the development opportunity. We are doing ours in tandem.

“Long Marston near Stratford-upon-Avon is still a live project. We’ve been working with CALA Homes, which has half the former RAF site. It has a rail link. They are going through the process at the moment to see how it could work - they’re at the stage we were ten years ago, but it could work much quicker there.

“There’s also an attempt to develop Bordon in Hampshire linked to reinstatement, but Network Rail hasn’t offered a lot of support, so that will more likely go ahead without the transport infrastructure.”

So why has Tavistock been a one-off? Frost offers this analysis:

“Network Rail is a rail operator, not a property developer. It has looked at partnerships to redevelop station assets, but not the wider opportunities. It has such a huge property asset base - it has almost limitless potential. So far it has targeted the obvious and best opportunities - King’s Cross, Waterloo. It probably doesn’t have the time or manpower to set up more joint ventures.”

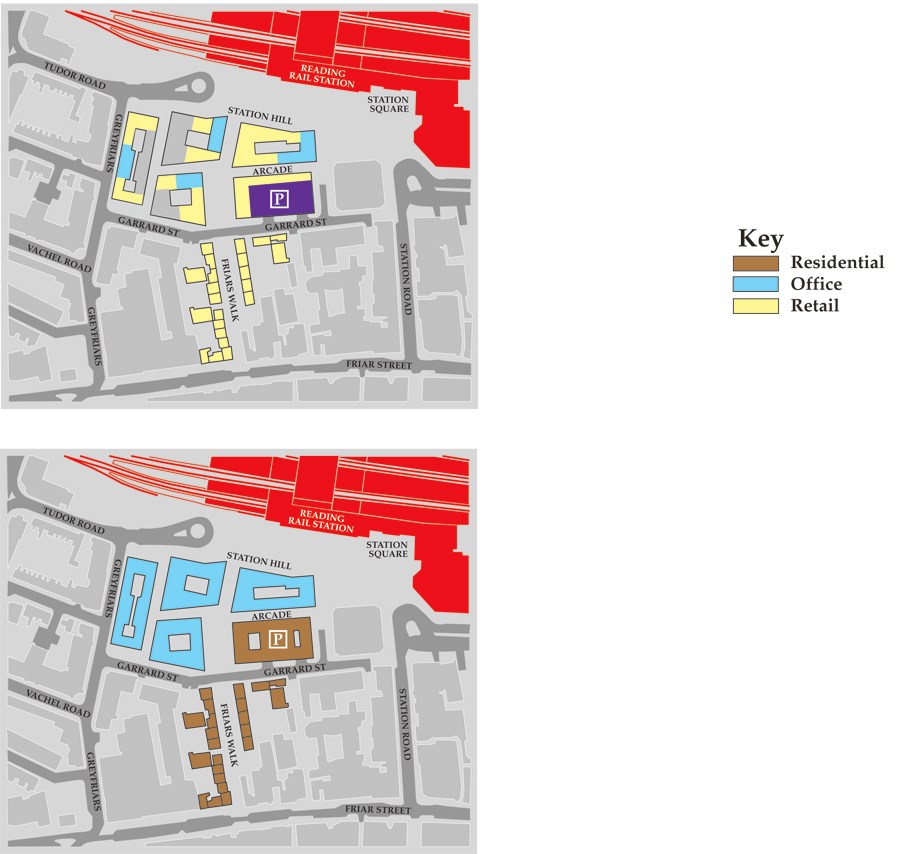

Case study: Reading

Reading’s new station is almost complete. Her Majesty the Queen opened the station last July, and a ten-day blockade over Easter will bring the final parts of this five-year, £950m transformation into use. Yet around the station, the arid urban landscape is in desperate need of modernisation.

“Reading Borough Council has been very proactive,” defends Labour councillor Tony Page, deputy leader of the council and cabinet member for environment, planning and transport.

“We created a development framework for the station in 2002. It was Reading’s pioneering work that pushed the Department for Transport and the rail industry to provide a catalyst. Looking at it 13 years on, it was far-sighted.”

But the station still stands out like a sore thumb. Network Rail has played its part - by 2030, passenger numbers through the station are expected to double from today’s 15 million. So why has the local council yet to seize its opportunity to “do a King’s Cross”?

“Back in 2002 we called it an arc of renaissance, which sounds a bit pretentious now,” says Page. “But the area around the station is only freed up when Network Rail pulls out. That’s later this year.”

The Station Hill area promises 300 new “residential units” (most people would call them flats or apartments) as part of a “mixed-use urban area of character and quality, refreshing and interesting retail”.

That description comes from Sackville Developments’ assessment of its £500m scheme, which has been given the go-ahead after years of local wrangling. The developers claim Reading offers more than 200 trains an hour to London… just a little over-stated? Try knocking the last 0 off that figure!

The first phase will entail the demolition of unloved and run-down shops opposite the station entrance. There will be a new seating area in front of the station, in the style of an amphitheatre. And a refurbished car park will boast a five-a-side football pitch and running track on the top.

Although the new station was effectively ready a year ago, the first new office building won’t be up before 2016, and the project will take until perhaps 2024 to finish.

“Without that huge investment in the station, it is inconceivable that this scale of redevelopment could have come forward,” argues Page.

“There would have been some regeneration, but nothing like this. The station was the crucial bit, developed on the assumption of doubling footfall.

“Those companies investing in Reading now have the confidence that the railway will be able to deliver the passenger flows needed to justify the investment. Because we took the initiative, we bought ourselves a seat at the table in a way no other local authority was doing at that time. We sat with Network Rail, the DfT and the train operators on an equal footing for the redevelopment.

“In terms of the public realm, we’ve had to wait. A lot of the area around the station has been the contractors’ building site. So a lot of the stuff for which we are paying could only be started once the station was done.”

Property values, he says, have gone through the roof, with the council believing that the station investment has fed through to inflated house prices. The extension of Crossrail to Reading and the expectation of a new service offering four trains an hour directly into Heathrow from 2021 have contributed to that. It has been critical to developers’ decisions to buy sites north and south of the railway line.

“Now, of course, electrification is joining up the dots,” says Page. “It is not unconnected that a Thai consortium has just bought Reading Football Club. Their mantra was that to reach the best development sites, you land at Heathrow and turn left to Reading, instead of turning right into London.”

Rail architect Paul Beaty-Pownall is more critical: “Reading station is a lovely architectural creation, very clever. But I can’t see its relationship with the town centre. It doesn’t face the town. There’s no connectivity with the shopping area, the town hall, the bus station. There’s no joined-up thinking.

“Birmingham New Street also seems very inward-focused - a fantastic new environment without a relationship with the city around it.

“These two projects are driven by Network Rail. From a national infrastructure point of view they are essential. But it’s all about the additional platforms to handle extra services. They’re not driven by any relationship with the communities they sit in, because that’s not Network Rail’s business driver.”

Two stations up the line from Reading is Oxford. It too has big plans, with a new Chiltern Railways service via Bicester to London cleverly branded as the first new inter-city route in a century.

“Network Rail and the Department have additional problems there, because Oxford’s not a unitary authority,” cautions Page. “They have to deal with the city council as planning authority and the county council as the highways authority. They have different agendas. There’s a parish council in there, too. Reading could speak with one voice, where Oxford cannot. There are tensions around that project that we never had.

“The lesson for others is that councils have to take the lead. Network Rail is not hot-wired for partnership working. You have to work at it. Network Rail has a big task just co-ordinating all the bits of its own empire, so to get it to work with outside areas requires a lot of effort. People who’ve spent all their working lives on the railway don’t necessarily understand what a council can do for them.

“Without being critical of individuals, with the station project we saw a lot of people who were very focused on delivering an important piece of engineering. The noise, the dust, the pollution, the movement of stuff to the site was ancillary to them.

“They’ve never seen us as the enemy, but at the start we weren’t necessarily friends either. We had to do our lobbying through Government separately, to make sure that all our ducks were aligned. Mind you - I shudder to think what it would have been like if we had still been dealing with Railtrack!”

The view from Hong Kong

Hong Kong railway operator MTR, which today runs London Overground and will soon take on Crossrail, first tried to enter the UK through a bid for South West Trains in 2006.

It wanted to export MTR’s successful way of working - a model that it called “rail plus property”. The corporation was handed parcels of land, which it developed. The profits were then used to fund the railway line. Typically, high-rise developments stand on massive concrete plinths above railway stations.

UK Chief Executive Jeremy Long wanted to apply the same principle in the UK, at stations such as Clapham Junction.

“In Hong Kong the model has continued apace. We show interest here - we’re still trying to find a way of structurally getting involved in rail property outside our concession, where we are not the franchisee. That’s still difficult to achieve.

“We carry out works for Transport for London on almost all the Overground stations. But where Network Rail is the freeholder and others are operators, it has proved difficult to find a structure that allows separate commercial development. Where a train operator is a leaseholder for only a small number of years, most people think commercial development has not happened as far or as fast as it could have done.

“In Hong Kong we start out as master planners of a community. We look at the community first and the transport second. But the plots of land are much larger, the spaces here from Network Rail are more limited.”

Argent’s Gibbs sees little similarity between the Hong Kong and UK rail models: “MTR is a property company which runs some trains. The property and the railway go hand in hand. They see the railway as something which makes the land more valuable.”

Network Rail’s Biggs says the Hong Kong model is not transferrable to the UK, also citing the example of Clapham Junction.

“Clapham is clearly a problem: a complex railway with very large footfall. We should be adding value by building above, but it is very difficult to get commercial schemes like this to stack up. To pay for a new station with a big concrete raft over it requires all the money up front, ahead of any development. The numbers generally do not add up.”

Long notes: “Land near railways in the UK was often low value. There was steam and dirt. The railways were unattractive places to live nearby, so they were poor. As trains have cleaned up - and particularly been electrified - stations themselves have lost the smoke and smut. And property around a station has gone from being cheap to more expensive, more desirable.”

Future development around stations

“In 20 years we won’t use station buildings the way we do today,” asserts Paul Beaty-Pownall, who is director at bpr architects, and who has spent the past 15 years preparing station strategies for train operators, exploring how they ensure stations remain fit for purpose.

“Customers will be fully supported by mobile technology. And a lot of things that happen in station buildings now will happen on board the trains instead. So do stations really meet the future needs of customers? As architects we do a lot of station enhancement. But we’re up against the limited funding allocated to stations as part of a franchise bid.”

Beaty-Pownall is talking about the medium-sized stations that are at the heart of cities such as Exeter or Oxford, buildings that he says are very important to the communities they serve but which are not central to the train operators’ business plans because they contribute little financially.

His firm has designed stations at Hassocks (for Southern) and at Wolverton (funded by Milton Keynes Council), and has recently submitted a planning application for West Hampstead station for Transport for London.

“Train companies get a return from passengers buying tickets, so they invest in that. They get a return from running trains up and down. But it’s hard for them to spend money on a station building in the context of a short franchise. They won’t make a return on it.”

There has been a big push to expand retail to get some revenue from the buildings. This is tinkering at the edges, he says.

“Their function serving the railway has perhaps had its day. So we have to get stations to turn around, to face their local communities. For the people nearby, they are really important - most other public buildings have already gone, or are targets for privatisation, but stations will remain public buildings for a long time.

“Station user groups have immense passion and energy. They’re often more passionate about them than they are about the trains themselves, and certainly more passionate about them than train operators are about their own buildings.”

Beaty-Pownall questions whether the right people are in charge of smaller stations. To the train operators they are a liability, rather than a source of revenue. Over the next decade, could they be transferred to organisations that could help them serve other purposes as well, attracting more people - and not just as passengers?

“Passengers’ experience now starts on a website,” he says. “They buy their tickets, get their information, plan their journeys. They move from the home to the train by some other transport, and would like to get straight onto the train, with all the information they need on their mobile device, reinforced by further information on board the train.

“The only point they need the station building is if they are in the minority of passengers who do not make that journey regularly, and need additional support.

“The station building has not yet had its day. But that time is coming. We expect very significant growth in passenger numbers. A lot of the obstacles that are currently in the way of passengers will have to be removed - gatelines, fences, buildings. The challenge is to adapt old buildings to accommodate that growth, given the lack of return that companies get from them.

“If you spend £10m on the area round the station, the local community benefits. It draws people in, property values increase, and the public realm improves. But the rail industry doesn’t necessarily gain much from it. So station development needs to start locally - local developers with local authorities driving it, because they are the ones who benefit from it. The rail industry does not need to contribute to it if it does not get a benefit.”

David Hunter, who has responsibility for station design at Atkins, says: “Network Rail is doing a lot more to collaborate with developers than ten or 15 years ago. But it could do more. We all acknowledge that. People demand more from stations now.

“But win-win partnerships have been difficult to find, because just putting some shops above the station is not going to fund the level of work Network Rail wants to achieve.”

NR’s Biggs comments: “At Epsom we set up a joint venture with Kier Property called Solum Regeneration. There was a commercial redevelopment - 116 flats, a Travelodge and three retail units - which funded a brand new station. It was all on land the railway needed. We just built above it.

“At Haywards Heath at the moment there is a bleak car park that needs expanding. We are putting in a significant increase in parking by making it multi-storey, and then bringing in Waitrose as well, which will fund station improvements.

“But these ideas are getting harder to spot. My job is more difficult now because we carried 1.6 billion passengers last year, up 50% on a decade ago. We are now planning for two billion in 2020. And new trains always seem to need new depots.”

Beaty-Pownall continues: “With increasing passenger numbers, as travellers we want to get through a station quickly. We don’t want the airport or Ikea culture, where you zigzag through retail areas to reach your train. So retail has to be a convenience, not a hindrance, generating money without obstructing. Waterloo has done that.

“There is less reason to do administrative tasks at a station now, like buying tickets. But there are more reasons to stay. I hold meetings at King’s Cross - we meet in cafés rather than offices. The reasons for using a station are changing. We want an environment for socialising and doing business. So stations can be destinations in their own right - getting a train isn’t the sole reason for being there.”

But does this just apply to the handful of major stations run by Network Rail, with their tens of millions of passengers a year?

Atkins’ Coburn says: “Network Rail used to have a reputation for doing nothing with fantastic sites, slow and uninterested in contributing to the areas in which it had properties. Now things have changed. There is good liaison with local authorities. But this is focused largely on the stations it runs, not the vast majority of stations run by train operators.

“The franchise documents control how much train operators are incentivised to develop stations. Contractual obligation tends to be at a minimum level. It is harder on a short contract to work with local councils. But there are some places where there is enough incentive, such as a new station for Cambridge Science Park.”

Beaty-Pownall adds: “Network Rail finds it difficult to communicate with local authorities. And local authorities find it difficult to communicate with them. With the devolution of Network Rail into route groups, I have quite high hopes that can improve. Locally is where these conversations need to start.”

Biggs reckons 250 railway stations can support what he calls “a retail offer”. Outside the major stations run by Network Rail, he says that is for the train operating companies to manage. And the remaining 2,250 stations have no commercial facilities.

“But there is a huge amount of value our transport hubs can generate with developers,” he concludes. “The value is in urban living, places of convenience where people want everything on the move - drop-in business lounges. We need to provide environments that encourage people in. Our customers are very interested in the built environment, and we need to meet their rising expectations.”

The last word goes to Beaty-Pownall: “Train companies are now beginning to see local transport partnerships as part of their strategic planning. But we are only going to see this taking shape in the next round of franchise awards, because it’s not encouraged in the current ones. Any franchises currently running have been given no incentive.

“People are now becoming drawn to the areas around stations, instead of to their cars on the ring roads. For a long time town centres have had stations in their back yards. The front door has been the motorway, the ring road, the multi-storey car park. That trend is reversing.

“Property values around the station are going up again, as property values around the motorway junction or circular road are starting to go down. So the civic space and the value of stations to the urban realm is increasing. There is a new opportunity.”

Peer review: Phil Gaffney

Peer review: Phil Gaffney

Non-Executive Director, Crossrail

It is both interesting and disappointing to note the conflicting views from the contributors to this article. Richard Coburn states that “railway companies and city regions have conflicting objectives” and that railways are only interested in getting people on/off trains as quickly as possible. Paul Beatty-Pownall’s view is that the railway station has a vital role in creating an urban realm which can benefit the local communities.

I am very much persuaded by the views of Paul Beatty-Pownall, particularly with regard to the need for the station configuration to be more outward looking and welcoming to the local community, and become a hub for social and business activities.

Opportunities for such station regeneration in the UK are plentiful, but the overriding thrust of the article is that it is difficult to do. Some of the reasons given are valid, such as the short term of operating franchises and the need for Network Rail to focus on the large developments. But such difficulties can surely be overcome, and obviously have been in certain places. The key factor common to these successful examples is when all parties involved work in a collaborative way.

At the other end of the scale, the issues associated with mega-projects such as King’s Cross appear to be no less difficult, which indicates that access to funds is not the major barrier to delivery.

The planning and delivery of a new railway such as Crossrail or HS1, or remodelling of major urban stations such as Birmingham New Street or Reading, offer opportunities to develop and deliver a built environment that not only meets the transport needs of the City or Region, but also contributes to the social and economic infrastructure of the area it serves.

The article considers the Hong Kong MTR experience, and Jeremy Long and Andre Gibbs explain how difficult it has proven to be to export the Hong Kong Rail plus Property model to the UK railway environment. While the Rail plus Property funding model may be difficult to achieve, I would argue that the UK would welcome the outcome of this model both in terms of the integrated mixed use developments built around the railway stations and the positive effect this has on railway patronage.

The next two decades in the UK will offer major opportunities for large-scale property developments associated with railway projects - Crossrail, Thameslink, HS2, Crossrail 2. It is essential that the sponsors of these projects consider the potential benefits from property developments associated with the railway, and for the delivery organisation to be sufficiently resourced to work collaboratively with the Local Government bodies, other agencies and property developers to ensure that the completed project offers seamless integration between the railway and the districts it serves, adding value to those districts in terms of employment, residences, retail and leisure.

Crossrail is an example of what can be achieved in moving towards the Hong Kong model, even with the constraints noted in the article. As an integral part of the project, Crossrail has integrated the design for 12 major property developments over and around its central London stations and other key infrastructure. Development plans cover over three million sq ft of office, retail and residential space between Paddington and Woolwich. It is anticipated that this will generate £500 million income, with this forming part of the Crossrail funding strategy. Modest by Hong Kong standards, but still a significant and welcome contribution.

Peer review: Mike Goggin

Peer review: Mike Goggin

Director, International & Advisory,

Steer Davies Gleave

It was coincidental that on the weekend I read Paul’s article, the Sunday Times carried a piece on the work of Related Developers and its massive redevelopment in New York City (Hudson Yards), and its teaming with Argent (the developer behind King’s Cross Lands). Clearly the railway in Britain continues to have interest and merit, despite the difficulties alluded to in Paul’s article.

I have had the pleasure of working with GB’s railway stations from the very outset of my career, and have had the pleasure of working with developers, architects, local activitists, operators and station staff. And Paul’s article touches on some ‘home truths’ for those of us involved with the railway and its stations.

All too often stations are viewed from a single perspective – commercial, asset, operational. In the work Steer Davies Gleave is doing for the Rail Delivery Group, we are helping it to establish a broad set of principles that consider the role and impact of a station more holistically. When finalised, I hope it will recognise that a station arguably needs to be considered as 50% railway and 50% community. Recognising that the backyard of our stations touches the everyday lives of our communities, and working with them, will produce benefits for all parties.

Richard Coburn rightly notes that there can be a tension between a railway operator’s wish to move people quickly and a community that might want stations to offer additional value. However, I don’t think this is the major issue driving any sub-optimisation - after all, creating a place attractive enough to encourage dwell encourages retail spend that benefits the operator. In my personal view, the owners and operators of stations need to:

- Create a sense of ambition – there needs to be a shared cultural aim to make the best of the estate for the railway and the community it serves. From my conversation with Peter Wilkinson, the man leading franchise development for the Department for Transport, he clearly wants to see bolder and more innovative approaches to the use of stations and other property. I hope that our work with RDG and its engagement with industry stakeholders starts to ‘lift the heads’ for the potential of the estate.

- Engrain the holistic perspective from the outset – at the very heart of the industry’s franchising and Periodic Review process, there needs to be a more visible consideration of the broader benefits to the local and UK economies of station-related property development. Alongside the funding assumption that ORR determines for Network Rail’s property, there needs to be a broader recognition in its licence (and ultimately its Delivery Plan) as to how development is conceived and delivered. This could lead to tension between ORR and Network Rail because community-engaged development might take longer or cost more, but at least it recognises the reality of the railway’s integration into the communities it serves.

- Industry understanding – the good news over the past decade is that the UK Government has put a lot of money into the railway and into its station estate. I would argue that the industry has not yet done enough to pool its learning and insights, to find out what worked and what didn’t.

In a tougher financing environment, and where funding is likely to come from multiple sources, the industry needs to be able to articulate and tailor the case for investment to leverage those funds. SDG’s research for Network Rail into station investments found cases where the benefits might be understated in traditional transport appraisal terms by five to seven times.

The industry also needs to ensure that if industry-wide schemes are developed (for example, National Stations Improvement Programme or the ‘onward travel poster initiative’ that ATOC committed to in 2010), that they are efficiently deployed and effectively sustained. Some mature decisions over prioritisation and the extent of devolution may be required.

- Management capability – it is quite clear that there are pockets of management where any signage is considered good, where the solution to increasing retail spend is to ‘pile it high’, and where follow-through on station investments is poor - for example, poor-quality seats on the mezzanine at King’s Cross and failures to update Stations Made Easy at other stations. There continues to be a significant churn in the people managing the stations on a day-to-day basis - the industry can do more to recognise that station management is a taxing role that brings together multiple skills and perspectives, including human resources, safety, commercial, operational, retail and design. ‘Professionalising’ station manage-ment within the structures and competences would bring benefits.

- Sustained determination – previous attempts at contractual reform is a story of valiant efforts to recognise the fact that the original leasing and access structure created at privatisation was overly complex, inhibited change and led to documentation that did not reflect reality. Unfortunately, those efforts met with limited success (and sometimes no success) as proposals for reform, developed over many months, were then dropped. The industry needs to ensure that there is clear, sustained momentum and a shared accountability for making real change to the processes that govern station management and development.

I have so far focused on the station estate. However, the railway network extends far beyond station lease boundaries. What then for optimising the rest of the estate?

I do think we need to recognise both the challenges and the potential. The challenge of building adjacent to, over or re-using railway estate for development shouldn’t be underestimated. Network Rail and train operators are rightly concerned to ensure that delivery of the development doesn’t have an impact on the safety or efficient ongoing maintenance of the railway, both during construction and when completed. This principle, I would suggest, would be endorsed by all parties involved.

It is therefore the execution of the arrangement where challenges and complexity arise. Perhaps it is time to look again at how Asset Protection Arrangements are conceived and communicated to potential interested parties. The industry needs to remember that, with the Government’s planning changes, there are now more places away from the railway where development can occur. These places often have a simpler structure of participation, a lower time for development and cost of construction, and avoid some risks such as contamination.

In terms of potential, the railway estate is well placed to meet community needs for additional housing. To coin a phrase from the US, ‘transit oriented development’ is something that the UK industry has developed successfully. With work under way to develop generic and lower-cost approaches to decking over railways and to adjacent development, perhaps we can see some of the blighted carriage sidings and maintenance depots brought back into life.

However, to achieve this with confidence and determination requires a detailed and mature discussion on the future of the railway network and its services - I would argue that it begins and ends with a clear and shared understanding of what the railway network, its stations and its train services are there to deliver.

Peer review: Laura Kidd

Peer review: Laura Kidd

Head of Architecture, HS2

In my view, the question is not whether the railway is making the most of its development land, but whether the railway understands its role in providing the best possible places for people to live and work, in and around its stations.

From large city interchanges to small stations, transport hubs are a central focus for the places that they serve. Railways are there to provide a service to their passengers, but these passengers also live and work around the stations. There should not be an isolationist approach - the best transport designs and developments have people and places at their heart.

The relationship between station owners, developers and local councils is the key to maximising prospects for the public realm. I also think that local councils are best placed to take the lead, but with some smaller councils being limited in their resources and experience, developers and station owners may need to assist them in developing the best opportunities.

Lessons are being learned, and this is evident from the cited case studies. Things that were acceptable 20 or even ten years ago would not pass muster now. One of the aspects of St Pancras station that could have been better is the public realm around it. The Barlow Shed is a splendid landmark, but at street level more could have been done to activate the station facades and provide a more permeable and integrated public realm. A fully activated and integrated public realm not only makes people feel safer, it is safer.

Stations, especially large to medium-sized ones, are first and foremost in the public realm. They can positively influence their surroundings to make places work better for passengers and local people. Manchester City Council has taken the opportunity of the forthcoming HS2 station in Piccadilly to drive a development scheme for the area. Similarly, this is happening with the GLA vision for Old Oak Common.

Council involvement can help to ensure that the development is not just about financial returns. Councils can help drive the vision for a development that will provide the optimum mix of public and private buildings and local amenities, alongside integrated and intermodal transport plans.

The integration of over-site development into a station’s design raises many issues. Air space above stations, especially in high-price property areas, is seen as a good development opportunity, although building over a railway always adds additional costs. If the development is over the concourse and platforms, the station will have to take the often significant structure of the development into its operational realm. This isn’t a problem for deep metro stations, where the separation of the railway is far removed from the development, but for surface stations, this potentially has two negative effects. When change is proposed - especially rebuilding or refurbishment - there will always be an interface that the station must manage, and that may have an impact on the passenger experience and perspective.

Additionally, we have cultural expectations for our railway stations - the historic idea of an airy, light train shed is quite deep in our psyche. Over-site development must be designed to mitigate these conflicting needs and potential negative impacts.

Peer review: Graeme Craig

Peer review: Graeme Craig

Director of Commercial Development, TfL

The key realisation in developing our commercial strategy was that Transport for London is a property company. Of course, property will never be the most important thing we do, not when there are 30 million journeys on our network every day. We do, however, have 5,700 acres of land and over 400 potential development sites, so we are a property company whether we like it or not, and a large one at that.

It begins, of course, with the stations - the places that are (or should be) much more than where people get on and off trains. With more than four million journeys on just the Underground every day, stations are often the most convenient place for our customers to pick up the things they need, which is why we have rolled out ‹click and collect› at 43 stations in a little over a year.

The next step is to recognise that we can invest our assets to deliver the housing and employment that London needs. What is more, we are building on transport nodes, the very place where it is most efficient to place development. Integrating our commercial and operational plans, we can enhance our stations, providing step-free access and other improvements for both customers and staff. All this, while generating substantial revenues (over £1 billion from development alone) that we can reinvest back into the wider transport network.

The really interesting thing is that each station is not just an entrance to the rail network, each station also acts as a gateway to a different part of the capital. And that is important because London is not a single, uniform city. It is made up of multiple cities, towns and villages - and people’s experience of each part often starts when they get off a train onto one of our platforms.

While there must be a design that runs through the whole network, every station and every station development should ideally reflect the environment of that part of London. Customers should have a sense of where they are in London without seeing the station name.

To take forward over 50 development opportunities across the capital, we recently launched our Property Partnerships. We are looking for a small number of partners who will work with us over the next decade to deliver a series of developments that will transform London. Our objective is to deliver long-term income through high quality development, working alongside partners who care as much about London as we and our customers do.

We will need a range of partners, given that our potential developments include listed buildings with opportunity for residential conversion, mixed use and residential developments over stations and depots, major regeneration schemes in urban centres, and brownfield developments in inner and outer London. By having only a small number of partners, we can take learnings from project to project, and also build teams of people who get used to working together.

We do need to take the time to work through the right answer station-by-station. This builds on recent work where we had more than 1,700 local people involved over six months in helping us design a new development at the heart of Northwood.

With such a fantastic portfolio, the biggest mistake we could make is to forget that the reason why TfL exists is not to develop its property. Fortunately we have 30 million reminders every day that our primary goal is, and always will be, transport.

, stands at Peterborough on April 8 2023. The ‘90’ has been acquired by Freightliner from DB Cargo. PIP DUNN.")

, stands at Peterborough on April 8 2023. The ‘90’ has been acquired by Freightliner from DB Cargo. PIP DUNN.")

Login to comment

Comments

No comments have been made yet.